The Dodd-Frank Act and Small Bank Creation†

Kim J. Ruhl

Mary Sue and Mike Shannon Chair in Economics, UW–Madison

May 15, 2019

In response to the U.S. financial crisis of 2007–2008, the “Dodd-Frank Wall Street Reform and Consumer Protection Act” (henceforth, the Dodd-Frank Act or just the Act) was enacted on July 21, 2010. This sweeping reform was meant to stabilize the financial system and prevent future crises. A major component of the Act was the increase in capital requirements and regulation of bank activity.

Several authors (Liu, 2019; McCord and Prescott, 2014; Peirce, Robinson, and Stratmann, 2014) have argued that the Act has increased regulatory costs for banks and that these costs are largely unrelated to bank size — for example, a bank may need to hire an additional full-time employee to manage regulatory compliance. These fixed costs would be a larger burden on small banks, impacting profitability and dampening entry of small banks.

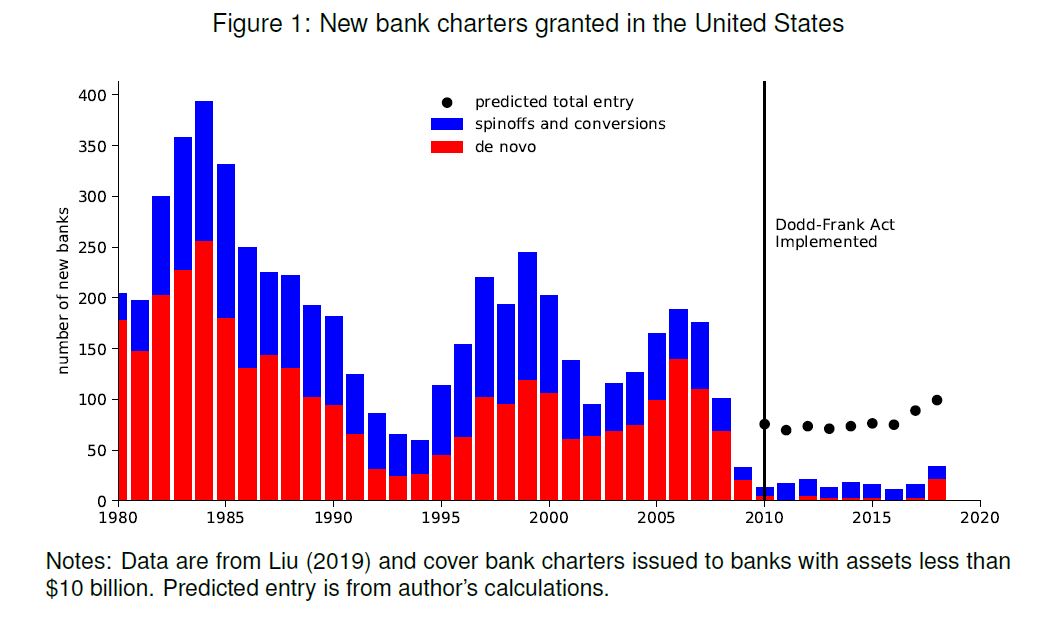

Figure 1: New bank charters granted in the United States.

A decline in small bank creation is particularly concerning for small businesses and rural communities. Small-business financing often takes the form of “relationship lending” in which the loan officer plays a key role in determining the credit worthiness of the firm. Small banks are best suited to this type of lending (Berger and Udell, 2002), and a decrease in their viability would impact the flow of credit to small businesses. As we show below for Wisconsin, small banks are important sources of banking services in rural counties, which tend to be relatively poor. A decline in small bank creation is likely to affect disproportionately these under-served areas.

In Figure 1, we plot the number of new small banks created per year in the United States. We define a small bank to be any commercial bank with assets less than $10 billion. Before the passage of the Dodd-Frank Act, the creation of new banks was strongly procyclical: Small bank creation is high during expansions and low during recessions. On average, 181 small banks were created per year from 1980–2009 and 57 percent of these new banks were de novo, meaning that the new bank was not the result of a spinoff or a charter conversion.

In the years following the passage of the Dodd-Frank Act, the creation of small banks has all but ceased. The average number of new small banks per year falls to 18 in the period 2010–2018. Of the 159 banks created in this period, only 38 (24 percent) of them are de novo entries. Given the severity of the recession, it is not surprising that bank creation is low from 2007–2009, but the post-2009 economic recovery has not been accompanied by an increase in small bank creation.

To get a sense of the “missing” small banks, we estimate a simple model of small bank creation. Using data from before the passage of the Act (1980–2009), we model small bank creation as a function of the Federal funds rate (a proxy for the return on assets) and the growth rate of gross domestic product. We use the estimated model to predict small bank creation for the period after the enactment of the Dodd-Frank Act. While the predicted level of bank entry is low relative to the past — interest rates are historically low in this period — the model predicts significantly more bank entry than we observe.

The simple models predicts that 704 small banks should have been created from 2010–2018, compared to 159 in the observed data. Of the new small banks we expect to observe, only 23 percent of them have been created.

Small banking in Wisconsin

We turn next to the Wisconsin data. In 1980–2009, Wisconsin accounted for 1.3 percent of small bank creation. If this share was the same in 2010–2018, an extrapolation of our simple model predicts that Wisconsin should have seen about 7 more small banks created since 2010.1 In 2009, there were 245 small banks in Wisconsin: The missing entry accounts for almost three percent of the stock of small banks.

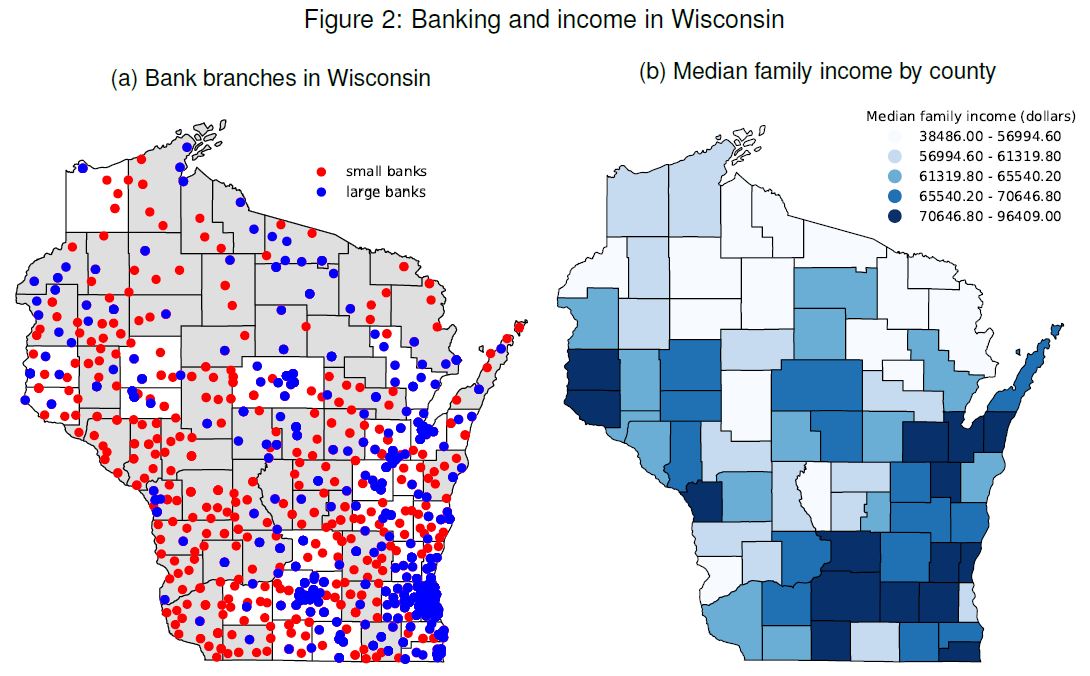

Changes to the small banking industry are particularly important for consumers and businesses located in poorer and rural areas. In Figure 2a we plot the location of every bank branch operating in Wisconsin in 2019. The red dots are branches of small banks (assets less than $10 bil.) and the blue dots are branches of large banks (assets greater than $10 bil.). The shaded counties are those denoted as rural by the U.S. Department of Agriculture.

Large banks are clustered near the metropolitan areas surrounding Madison, Milwaukee, and Appleton-Green Bay. Counties in the west and north of the state are much more dependent upon mall banks, and six counties (Buffalo, Florence, Jackson, Pepin, Monroe, and Trempealeau) are home to only small bank branches.

In Figure 2b, we plot median family income by county from the U.S. Census Bureau. A simple inspection of the two panels from Figure 2 suggests that low-income areas are less likely to host branches from big banks.

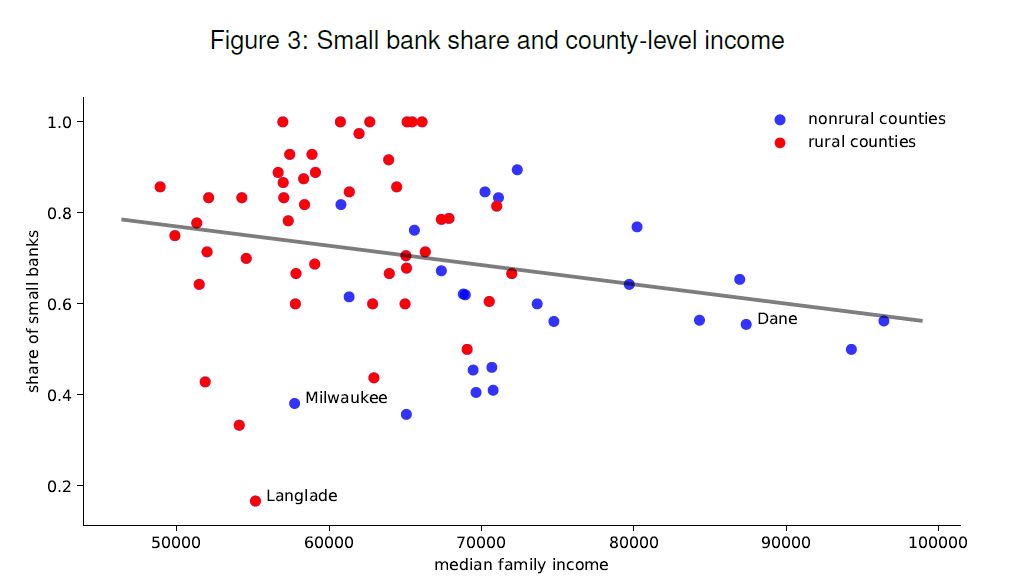

In Figure 3 we formalize the relationship between the importance of small banks, rurality, and income in Wisconsin counties. The vertical axis measures the proportion of all banks in a county that are small. This number ranges from 0.17 in Langlade county to 1.0 in the six counties that have no big-bank branches. The horizontal axis measures median family income in the county. This number ranges from $48,912 in Rusk county to $96,409 in Waukesha county.

From Figure 3 we can see the negative relationship between the importance of small banks in a county and the income of the people in the county. In addition, we have plotted the rural counties as red dots and the nonrural counties as blue dots. Small banks are clearly most important in rural, low-income counties.

Summary

Small bank creation has not rebounded to pre-recession levels even as the economy continues its recovery. Research has found that the burdens associated with the Dodd-Frank Act have been particularly hard on small banks and this is consistent with the data on small bank entry. Small banking is most important in poorer, rural areas, which suggests that these areas would be most affected by changes in the health of the small-bank sector.

References

Liu, Kuan (2019). “The impact of the Dodd-Frank Act on small U.S. banks.” Mimeo.

McCord, Roisin and Edward Simpson Prescott (2014). “The financial crisis, the collapse of bank entry, and changes in the size distribution of banks.” Economic Quarterly 100 (1), pp. 23–50. Peirce, Hester, Ian Robinson, and Thomas Stratmann (2014). How are small banks faring under Dodd-Frank? Working Paper 14-05. Mercatus Center.

Berger, Allen N and Gregory F Udell (2002). “Small business credit availability and relationship lending: the importance of bank organisational structure.” The Economic Journal 112, F32–F53.

†Data briefs are short, timely reports that use data to highlight economic issues of importance to policy makers, business leaders, and the public. This brief, and the data and code that underlie it, are available at crowe.wisc.edu. The views expressed herein are those of the authors and not necessarily those of the Center for Research on the Wisconsin Economy, the Department of Economics, or the University of Wisconsin.